Introduction

Investing can be daunting for some people. The topic itself is scary because there is a lot of uncertainty, but the majority of our audience is into dollar cost averaging (DCA). In this article you will learn a different way to invest your money by capitalizing on money you have in your employer sponsored plan. If you do not have an employer sponsored plan then it may be a great time to look into it because you may be missing out on potential financial strategies.

What are employer sponsored plans?

Employer sponsored plans are tax-deferred retirement accounts in the form of a 403b, 401k, or 457. For the sake of this article we will not explain the difference between them, but they do have distinct differences. Pre-tax money is deposited into one of these accounts from your paycheck depending on the percentage contribution you manually set. The capital deposited into this account decreases your gross income for the current tax year. Depending on how much you’ve contributed over the years, you may be able to unlock the ability to loan yourself money from this plan. The ability to do this enables you to make investing and saving easier for you.

What do most people do?

In a financial crunch most people will take a loan from a bank. Although this is normal for the general public, it may not be as beneficial as you think. When you loan from the bank, you have to pay interest to the bank and other fees associated with the generation of the loan. This is theoretically a wasted use of capital, but is sometimes needed in dire situations. Rates and terms for specific loans are dependent on the institution and are dependent on personal credit scores. Credit scores may be affected if the borrower defaults on the loan, which can lead to other detrimental effects in the future. A borrower may be denied access to capital if they default on a loan and may require consignment requirements or higher rates in the future.

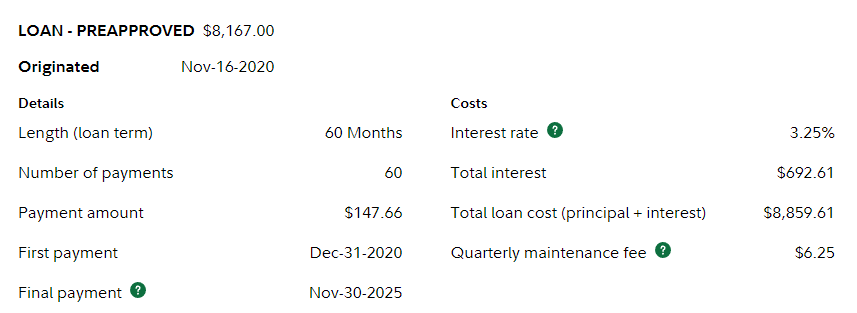

The benefits of loaning from yourself.

There are more pros than cons when you loan yourself money from your retirement. “Don’t touch your retirement” is what most people will tell you, but we encourage everyone to look into this strategy. Another way of thinking about it is that it is rarely ever a car’s fault for a car crash - it’s the driver. This also applies to finance. We will explore the pros of loaning money from your retirement and why the benefits outweigh the cons of traditional methods.

No credit checks

There are no credit checks because this is money you’ve earned from a working wage. Loans from your retirement are considered secured loans because they use your retirement funds as collateral.

Interest goes to you

Instead of paying interest to the bank/institution - all of the interest goes to you. In time you will increase the capital in your account, but loaning to yourself allows for no wasted capital. You keep everything in-house. The interest for this loan is usually less than what is offered at a bank/institution, which also helps with payments overtime.

You set the loan amount/term

This may vary depending on the institution that holds your retirement, but it is usually a 0-60 month term that will show the amount of payment before accepting. The max amount is dependent on the institution, but it is usually up to $50,000.

No Taxes***

Notice that there are asterisks next to the word taxes. If a loan is paid on time then no taxes will take place. If the borrower defaults on the loan then the amount loaned will count towards income, for the year, and will incur taxes. For example if you made 100k for the year, borrow 50k, and default on the loan. You will effectively pay 150k in income tax for that tax year.

How you can use this to your advantage.

Lump sum at risk price points

Simply put you can’t buy a house in 2008 at the price point that was deep into the recession. This allows you to take advantage as a value investor by setting your risk and capitalizing on opportunities that will possibly not present themselves again in the future. Of course this can be a double edged sword, but this is only to be used if you're an experienced investor that knows their risk management and investment thesis.

Flexible Investing/Payments

It allows you to have flexible monthly payments instead of dollar cost averaging. Consistently saving 500 dollars a month for a Roth IRA can be challenging for some people, but if you want to save and have the flexibility then this may give you that option. Of course you can take more or less of an amount, but this should help you either way.

Conclusion

Loaning from your retirement can be a double edge sword. We understand that there is some risk involved with this strategy, but market conditions may allow you to acquire assets at certain price points. There’s really no point in paying other banks/institutions when you can do everything yourself. Allowing yourself the flexibility to keep your own capital for emergencies, while loaning from yourself, will allow you to keep yourself in the market without ever having to stop annually investing. If you have any questions, feel free to leave them in the comment section below. Take care.

Retire By Investing is on a mission to help others increase their free time through financial education. This substack does not provide financial advice of any kind. We do not sell or manage financial investments or vehicles. We are not licensed individuals and are not liable for any financial decisions you make. Please do your own due diligence and consult/seek your financial advisor regarding any decisions. Thank you. Have a great day!

Thumbnail Pictures Provided By These Artists on Pexels.

Share this post